Results for the full year to 31 March 2023

Philip Jansen, Chief Executive, commenting on the results, said “Openreach is competing strongly and it’s clear that customers love full fibre. The Openreach Board has reaffirmed its target to reach 25 million premises with FTTP by the end of 2026 and plans to further accelerate take-up on the network. In Consumer we’re delivering for customers with strong growth in FTTP and 5G, and we’re also seeing green shoots in B2B with a return to revenue growth in the final quarter in Global and the creation of our newly integrated Business unit. “By continuing to build and connect like fury, digitise the way we work and simplify our structure, by the end of the 2020s BT Group will rely on a much smaller workforce and a significantly reduced cost base. New BT Group will be a leaner business with a brighter future.” |

Continued strong delivery against strategy

- We delivered revenue and adjusted1 EBITDA in line with our outlook for FY23, despite significant headwinds; normalised free cash flow was delivered at the lower end of our guidance range due to increased cash capital expenditure, primarily in Openreach

- FTTP build of 702k premises passed in the quarter at an average build rate of 54k per week, with 41% of our 25m build completed; FTTP footprint of 10.3m, up 43%, with a further 6m where initial build is underway

- Customer demand in Openreach for FTTP extremely strong with FY23 orders up 70% year on year; take up rate grew to 30.4% with record net adds of 395k in the quarter; base now c.3.1m

- Record quarter of Consumer FTTP connections up 50% year-on-year with the base now over 1.7m

- We have 8.6m 5G connections, up 62% on last year; our 5G network now covers 68% of the population

- Cost transformation on track with gross annualised cost savings of £2.1bn since April 2020 against our £3bn target, with a cost to achieve of £1.1bn against a target of £1.6bn

- Created Business through the merger of Enterprise and Global to enhance value for all B2B customers, strengthen our competitive position and deliver material synergies

- The UK Government announced a three-year 100% tax expensing benefit on qualifying UK capex, effective from 1 April 2023; this will allow Openreach to deliver increased connections and offset inflation whilst reconfirming our 25m FTTP target by the end of 2026

- New metrics announced to track our transformation into a next-generation connectivity provider (see page 4), focussed on our networks, our customers and becoming a more efficient organisation

- Total labour resource2 to reduce from 130k to 75-90k by FY28-FY30

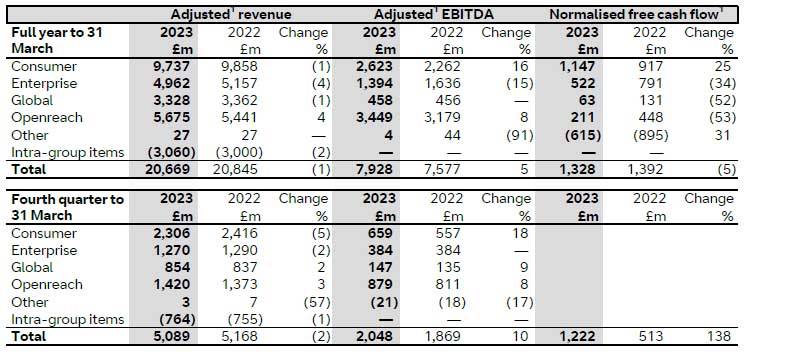

Pro forma full year revenue and adjusted1 EBITDA growth:

- Revenue £20.7bn, down 1% with the growth in Openreach more than offset by decline in the other units

- Adjusted1 EBITDA £7.9bn, up 5% due to growth in Openreach and Consumer offset by a decline in Enterprise

- Revenue up 1% and adjusted1 EBITDA up 3% on a Sports Joint Venture ('JV') pro forma1 basis

- Reported profit before tax £1.7bn, down 12% due to increased depreciation from network build and specific items, partially offset by adjusted1 EBITDA growth

- Reported capital expenditure ('capex') £5.1bn, down 4%; capex excluding Spectrum up 5% due to higher fixed network investment primarily in Openreach for building, and connecting more customers to, FTTP; cash capex was c.£0.2bn higher at £5.3bn (up 10%) as we reduced our capital creditors; significantly lower capex in Q4 given unwind of Openreach work in progress ('WIP')

- Net cash inflow from operating activities £6.7bn; normalised free cash flow1 £1.3bn, down 5% due to increased cash capex and adverse working capital movements offset by EBITDA growth and a tax refund; increase in Q4 due to timing of working capital, lower cash capex, and increased EBITDA

- Net debt £18.9bn, up £850m primarily due to pension scheme contribution of £1bn

- Gross IAS 19 deficit of £3.1bn, up from £1.1bn at 31 March 2022 mainly due to the impact of higher real gilt yields partly offset by deficit contributions

- Final dividend of 5.39 pence per share (pps) bringing the full year dividend to 7.70pps, flat year on year

- FY24 Outlook: revenue and EBITDA growth on a pro forma basis; capital expenditure excluding spectrum of £5.0bn-£5.1bn; normalised free cash flow of £1.0bn-£1.2bn

Customer-facing unit updates

Performance against FY23 outlook

1 See Glossary

2 Total labour resource includes both employees directly employed by BT and non-employees supplied by a third party

Glossary | |

| Adjusted | Before specific items. Adjusted results are consistent with the way that financial performance is measured by management and assist in providing an additional analysis of the reporting trading results of the group. |

| EBITDA | Earnings before interest, tax, depreciation and amortisation. |

| Adjusted EBITDA | EBITDA before specific items, share of post tax profits/losses of associates and joint ventures and net non-interest related finance expense. |

| Free cash flow | Net cash inflow from operating activities after net capital expenditure. |

| Capital expenditure | Additions to property, plant and equipment and intangible assets in the period. |

| Normalised free cash flow | Free cash flow (net cash inflow from operating activities after net capital expenditure) after net interest paid and payment of lease liabilities, before pension deficit payments (including their cash tax benefit), payments relating to spectrum, and specific items. It excludes cash flows that are determined at a corporate level independently of ongoing trading operations such as dividends paid, share buybacks, acquisitions and disposals, repayment and raising of debt, cash flows relating to loans with joint ventures, and cash flows relating to the Building Digital UK demand deposit account which have already been accounted for within normalised free cash flow. For non-tax related items the adjustments are made on a pre-tax basis. |

| Net debt | Loans and other borrowings and lease liabilities (both current and non-current), less current asset investments and cash and cash equivalents, including items which have been classified as held for sale on the balance sheet. Currency denominated balances within net debt are translated into sterling at swapped rates where hedged. Fair value adjustments and accrued interest applied to reflect the effective interest method are removed. Amounts due to joint ventures held within loans and borrowings are also excluded. |

| Service revenue | Earned from services delivered using our fixed and mobile network connectivity, including but not limited to, broadband, calls, line rental, TV, residential BT Sport subscriptions, mobile data connectivity, incoming & outgoing mobile calls and roaming by customers of overseas networks. |

| Sports JV pro forma | On 1 September 2022 BT Group and Warner Bros. Discovery announced completion of their transaction to form a 50:50 joint venture (JV) combining the assets of BT Sport and Eurosport UK. Financial information stated as pro forma is unaudited and is presented to estimate the impact on the group as if trading in relation to BT Sport had been equity accounted for in previous periods, akin to the JV being in place historically. Please refer to Additional Information for a bridge between financial information on a reported basis and a Sports JV pro forma basis. |

| Specific items | Items that in management’s judgement need to be disclosed separately by virtue of their size, nature or incidence. In the current period these relate to changes to our assessment of our provision for historic regulatory matters, restructuring charges, divestment-related items and net interest expense on pensions. |

We assess the performance of the group using a variety of alternative performance measures. Reconciliations from the most directly comparable IFRS measures are in Additional Information.

BT Group is the UK’s leading provider of fixed and mobile telecommunications and related secure digital products, solutions and services. We also provide managed telecommunications, security and network and IT infrastructure services to customers across 180 countries.

BT Group consists of three customer-facing units: Consumer serves individuals and families in the UK; Business* covers companies and public services in the UK and internationally; Openreach is an independently governed, wholly owned subsidiary wholesaling fixed access infrastructure services to its customers - over 650 communication providers across the UK.

British Telecommunications plc is a wholly owned subsidiary of BT Group plc and encompasses virtually all businesses and assets of the BT Group. BT Group plc is listed on the London Stock Exchange.

For more information, visit www.bt.com/about

*Business was formed on 1 January 2023 from the combination of the former Enterprise and Global units. It commenced reporting as a single unit from 1 April 2023, with pro forma reporting information to be produced ahead of BT Group’s Q1 FY24 results.